Invented by Brian Grassadonia, Jesse Wilson, Block Inc

Offline payment processing is a method of processing electronic payments without the need for an internet connection. This is achieved through the use of specialized hardware and software that can store payment information and process transactions even when there is no internet connection available.

The market for offline payment processing is driven by the increasing demand for electronic payments, especially in areas where internet connectivity is limited or unreliable. This includes rural areas, developing countries, and areas with poor internet infrastructure.

One of the key players in the offline payment processing market is Square, a company that provides hardware and software solutions for processing payments offline. Square’s hardware includes a small card reader that can be attached to a smartphone or tablet, allowing businesses to process payments even when they are not connected to the internet. Square’s software also includes features that allow businesses to manage inventory, track sales, and generate reports.

Another player in the offline payment processing market is PayPal, which offers a range of solutions for processing payments offline. PayPal’s hardware includes a mobile card reader that can be used to process payments using a smartphone or tablet. PayPal’s software also includes features that allow businesses to manage inventory, track sales, and generate reports.

Other companies that offer offline payment processing solutions include iZettle, SumUp, and PayAnywhere. These companies offer a range of hardware and software solutions that allow businesses to process payments offline.

The market for offline payment processing is expected to continue to grow in the coming years, driven by the increasing demand for electronic payments and the need for solutions that can process payments even when there is no internet connection available. As more businesses adopt electronic payments, the demand for offline payment processing solutions is likely to increase, creating new opportunities for companies in this market.

The Block Inc invention works as follows

The method includes receiving, by the first computing device and from the second computing and while the first computing device and the second computing are offline with respect to a transaction processing system, the first payment information including an identifier corresponding to the second user; sending, by the 1st computing device to the 2nd computing device while the 1st computing device and the 2nd computing device are offline with respect the transaction processing system. The method involves receiving, both by the computing devices and by the second computing, first payment data that includes an identification corresponding the the second user. Sending, by computing devices, to computing devices, while computing devices and transaction processing systems are offline, second payment data that includes an identification corresponding the the first user.

Background for Processing electronic payments in offline mode

In the above methodology, the device of the recipient and that of the sender must both be in ‘online mode. The transaction will not be complete until it has been processed. But, ?authorization delay,? The delay in online transactions can be attributed to a number of factors. These include an increase in latency on the network or a slower authorization process by a payment processor. The merchant may not be able to tolerate these delays during peak hours (for example, if there is a large queue and the merchant wants to prevent customers from being disappointed by a lengthy wait). The merchant may sometimes operate the POS Terminal in offline mode instead of online mode.

Some conventional technologies allow transactions to be performed in offline mode. The POS terminal stores payment cards and the transaction summary locally when it is operating in offline mode. After the POS terminal switches to online mode, the POS will batch all offline transactions together and send them on to the payment processor. In some cases, the POS terminal may not return to the online mode for several minutes, or even many hours. If the merchant’s POS terminal is not connected to the network, it will take a while for the POS Terminal to transition back into online mode. The merchant accepting the credit card offline will not likely learn that the transaction was unauthorized until the customer leaves the merchant’s premises. Network problems such as unavailability, latency or manual or automatic switching between offline and online modes based on other factors than network connectivity, or even power saving requirements dictated either by an app, device, or user can also interfere with the correct routing of payment requests to the card issuer or payment processor. In cases where immediate or near-instant transactions are desired, it can be difficult to obtain authorization, as the recipient may or not have Internet access at the time the transaction. The merchant could be at risk of not being paid for the item or service provided in offline transactions.

To avoid such risks, the technology disclosed herein allows for transfer of money (e.g.) between a payer (e.g. a customer) to a receiver (e.g. a merchant) through transfer and use a “payment proxy. In particular, when the device of the customer (such as a cell phone or a laptop) or that of the merchant (e.g. a POS or payment beacon) are offline (the “offline payment technology”). In relation to a system for processing payments. ?Online? Online refers to Internet-based communications. The term “offline” refers non-internet, short-range communication distance (less than about 100 meters) based communications. Refers to short-range communications (less than 100 meters), which are not internet-based. Examples include BLE and Bluetooth. In offline scenarios where there is a short-range network, both the customer’s device and the merchant’s device can pair up and exchange payment proxy. This is especially true when long-range networks are unavailable. The offline device is then completed by the first device to come online. In another scenario both devices will submit payment requests to the payment system on behalf of each other as soon as they transition from offline mode into online mode. The payment system processes the transaction, for instance, based on the chronological order of payment requests. If the requests arrive simultaneously, the payment system can use its knowledge base or stored rules to resolve the dispute.

As used in this context, the term “payment proxy” is to be understood as a payment identifier. Refers to an identifier for a payment, such as a name, driver’s licence number, email, phone number or any other identifier that is associated or represents the bank or financial account of a merchant, customer or recipient. In one example, a payment proxy could include an alphanumeric (or string of) character and a monetary indication (e.g. ?$?,, etc.). The alphanumeric characters are preceded by a monetary indicator (e.g.,?$?, etc.). The term “alphanumeric characters” is used. As used here, a symbol can be either a numeric (i.e. alphabetic) or a numerical (i.e. numeric). Payment proxy can initiate payment transactions by itself without the need for the customer to provide credit card or debit card information. Payment proxy can be integrated into web applications, messaging platforms, social networking platforms and forums. In one implementation, users register and create a payment proxy that represents their interest within the payment processing system or on their device. Users can also link their financial information (such as credit card numbers, bank account numbers, etc.). The payment proxy is assigned at the time registration. “Mobile payment applications that are stored on mobile devices or accessed through them can be used for such registrations.

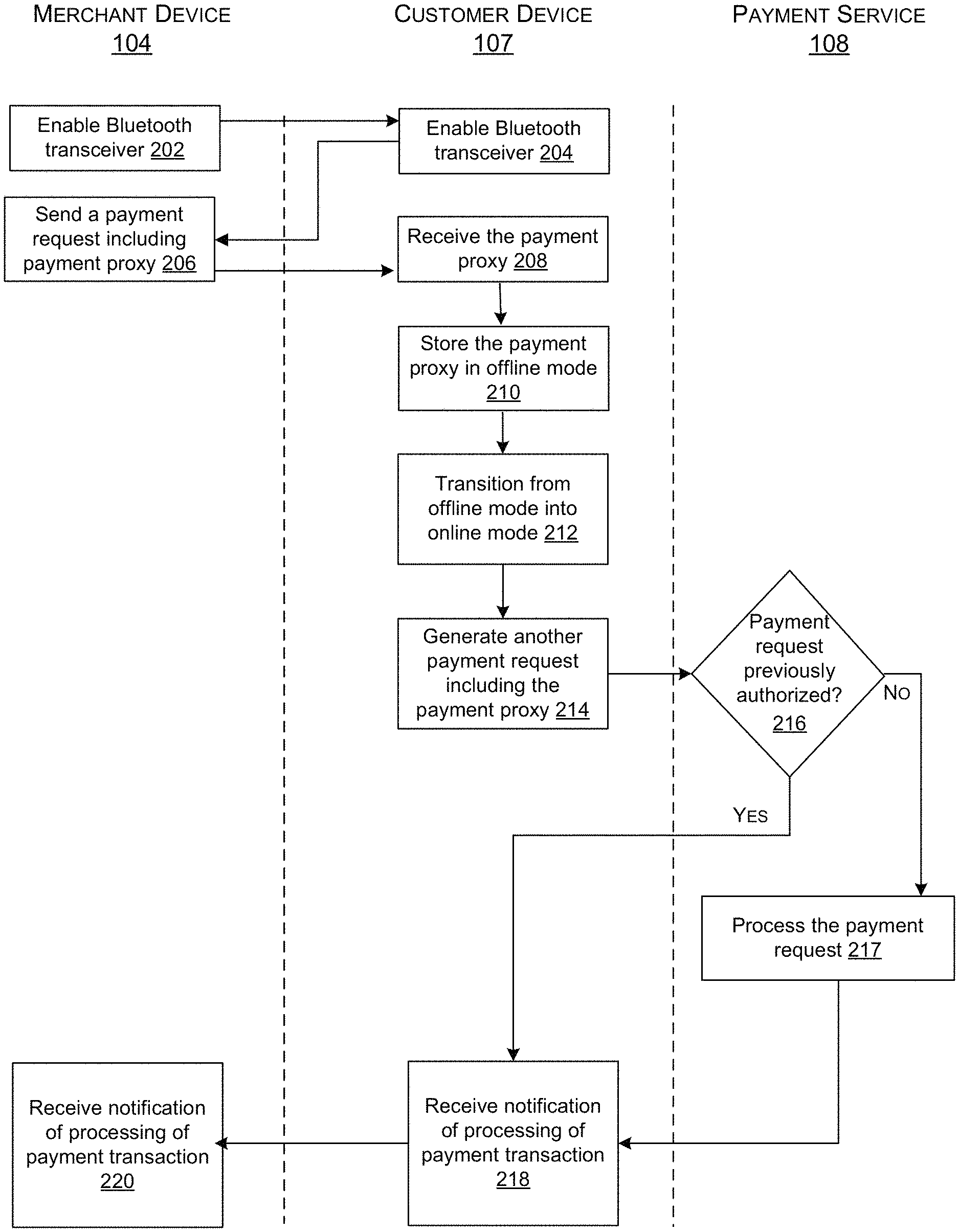

Briefly explained, a merchant using a merchant device identifies a second proximate device that is associated with the recipient or merchant (hereinafter referred as merchant device), e.g. a card-reader, a connected card-reader to a POS, a POS, or a beacon payment, all of which are counterparties in a transaction. Customer device or merchant device are offline in relation to payment processing system. Customer device and merchant device establishes a communication channel by using wireless technologies such as Bluetooth, Bluetooth Low Energy, Wi-Fi (or BLE), Radio Frequency ID (RFID), QR codes, Near Frequency Communication (NFC), or other wireless technologies. “An Internet connection is therefore not required to create a short-range communications field or channel.

The merchant device will transmit payment proxy through the established communication channel, which indicates the bank account or financial information of the merchant/recipient. Merchant devices can relay payment-related information, such as the payment proxy, to an external device on activation, for example, by responding to visual, audio, or tactile inputs by the user of a merchant or customer device. This is true regardless of whether there is a reliable Internet connectivity. “The customer device is also configured to receive/send payment proxy via the established communication channel.

Since the merchant device or either the customer device (or the card reader attached to it) can transmit or receive payment proxy, one of these entities can be an initiator or “primary device” “Since either the customer device or the merchant device (or a card reader connected thereto) can transmit and/or receive payment proxies, one of the entities can be the initiator or ‘primary device? The payment transaction. The term “primary device” is used in this context. The device receives the payment proxy and then generates, on behalf the other entity, a request for payment and submits it along with to the payment processing system. The “secondary device” The?secondary device?

In some cases, primary-secondary relationships can be set or fixed based on the user’s preferences. The merchant device, for example, is always primary and the customer device always secondary. In some cases, the primary/secondary relationship depends on which device goes online first. If the merchant device is offline and then transitions to online mode, the customer’s device will become the primary device. The offline merchant device remains as the secondary device. In another scenario, both devices initiate payment transactions. They also submit payment requests corresponding to payment transactions as soon as they establish network connectivity with payment processing system. Payment processing system then has to choose one request, discard the other or process both requests by transferring funds for the first request, and transferring “null” in response to second request. The payment processing system is then responsible for either choosing one request and discarding the other, or processing both requests by transferring funds in response to first request and transferring?null? The treatment of processing transactions can differ depending on which device, between the customer’s device and merchant’s device, is online.

The following scenarios will be considered. In the first scenario the customer’s device is off-line, but that of the merchant is online. In the second scenario the customer’s device is on-line, but that of the merchant is offline. “The offline payment technology described herein involves communication between a system authorized to process a transaction based on the payment request received by at least one merchant device or customer device which is online in relation to the system.

The merchant can then enter the received payment proxy into a dedicated field on a portal, e.g., a web application, an email application, a messaging app, a cloud application, a forum, a shopping form, a landing page associated with a uniform resource locator (URL) address, and/or like, which may be stored on or accessible via the merchant device, to create a request in response to a payment transaction for an item purchased by the customer from the merchant. The merchant may then enter the payment proxy received into a field dedicated to the portal. This could be a web-based application, email, messaging, cloud, forum, shopping form, landing page with an associated uniform resource locator address (URL), and/or similar. The merchant device may also automatically generate a request for payment upon receipt of the proxy. The merchant can specify through the portal a predefined sum that the sender is owed by the merchant. The merchant device that is online sends the payment request to a processing system and optionally sends an alert to the offline device to indicate that the request was submitted. In one implementation, a payment processing system may optionally parse payment proxy information of the sender or recipient and use a syntax-matching algorithm. The payment processing system will then communicate with an institution (e.g. an issuer or acquirer) in order to obtain details about the financial account that is associated with the payment proxy. Once the confirmation has been received from the institution, the transaction can be processed. A merchant server may maintain a database that includes information about financial accounts.

The customer can then enter the received payment proxy into a dedicated field on a portal, e.g., a web application, an email application, a messaging app, a cloud application, a forum, a shopping form, a landing page, and/or like, which may be stored on or accessible via the customer’s device, to create a request in response to a payment transaction for an item purchased by the customer from the merchant. The customer enters the payment proxy received into a field dedicated on a portal (e.g. a web app, email app, messaging application cloud application forum, shopping form, landing page and/or similar) that may be accessible or stored on the customer device to create a response to a transaction of payment for an item bought by the customer. The customer device may also automatically generate a request for payment upon receipt of the proxy. The portal allows the customer to specify an intent to transfer a certain amount to a specific recipient. The online customer device sends the payment request to a payment system and optionally sends an alert to the offline device (e.g. through a short range communication channel) to indicate that the payment request was submitted. In one implementation, a payment processing system may optionally parse payment proxy information of the sender or recipient and use a syntax-matching algorithm. The payment processing system will then communicate with an institution (e.g. an issuer or acquirer) in order to obtain details about the financial account that is associated with the payment proxy. Once the confirmation has been received from the institution, the payment processing system will process the transaction. A merchant server may maintain a database that includes information about financial accounts.

When both the merchant’s device and the customer’s device are offline, either one or both devices can be used as primary devices. In response to a transaction where the customer has purchased an item from the merchant, either device can receive or send payment proxy to another device. The primary device, which can be either the customer or merchant device, will send the payment proxy request to the payment system and, optionally, notify the other device that the request was submitted (e.g. through a short range communication channel). The payment processing system may then communicate with an institution (e.g. an issuer or acquirer) in order to obtain details about the financial account that is associated with the proxy payment. Once the confirmation has been received from the institution, the transaction can be processed. In certain embodiments, the merchant server can keep a database that includes information about financial accounts. In some instances, both devices can be online simultaneously. A contention component will then decide which device is to submit the payment request. The contention component will resolve the conflict based on various factors such as the risk scores of the devices and signal strength. In some cases the contention resolution can be fixed so that the payment system receives all requests but waits until a particular device (e.g. the merchant device) transitions into the online mode before submitting the payment request, regardless of when the transition occurs.

In a second case, when the first device enters online mode, it sends a notification that the second device can choose to not submit the payment request. In a third case, the system of payment processing resolves the dispute between two devices that submit payment requests. So, the two devices will submit the payment request for the other regardless of whether the other device is in the online mode or not. Payment processing system will process the request according to factors such as order of receipt, risk score, preferences set up by merchants or customers, time of day, payment amount etc. The payment system rejects the second request as a duplicate and sends an alert to the device that is receiving the first request.

When the customer device is online and the merchant device is also online, either one of the devices or both can simultaneously generate a request containing payment proxy information for the customer and/or the merchant, and send it to the payment system. The request will correspond to a transaction to pay the merchant for an item that the customer has purchased from the merchant. Payment processing system will then contact a financial institution to find out the details of the account that is associated with payment proxy. The transaction can be processed after receiving confirmation from financial institution. The payment processing system may choose to only respond to one request in the case of duplicate requests. A merchant server may maintain a database that includes information about financial accounts.

Some implementations described in this document also include techniques and arrangements that provide security and risk-rating functions to customers using mobile devices for transactions conducted offline. The security features protect the merchant against fraudulent transactions. In some embodiments the primary device, whether it is the merchant device or customer device, may be associated with a component for risk analysis. The risk analysis component may be stored on the customer device or the merchant device to determine the risk of the payment transaction. The risk analysis component calculates the risk based on previous transaction history. For example, the history of transactions between a customer and a merchant, or if there are any, the risk rating for the merchant that is pushed to the customer’s device with the payment proxy, which indicates the transaction “health” The risk analysis component determines the level of risk based on past transaction history, e.g., history of transactions between the customer and that particular merchant (if any), a rating associated with the merchant pushed onto the customer device along with the payment proxy (that indicates the transaction?health? The risk evaluation component then determines if the communicating device is trustworthy, and, if so, in certain cases, conditionally or provisionally authorizing payment transactions, for example, even when in offline mode. These provisional transactions will be confirmed once either device enters the online mode. In the embodiments described, multiple transactions can be batch-processed when the customer device or merchant device transitions to the online mode.

The embodiments described in the methods and system allow merchants and customers to conduct electronic payments even if their computing devices do not have Internet connections to process the transaction immediately. This allows merchants to do more business with their customers, without having to worry about maintaining a continuous network connection with the payment processing system. The risk analysis component allows for a reduction in the number of fraud transactions associated with a payment proxy based on past transactions or health metadata. This, in turn, indicates the level of risk that is associated with a payment object. The entire transaction process is convenient and seamless, even though the transactions are offline. This is especially true when a mobile payment object reader has been used. The disclosure includes several examples of payment capture techniques that are used in the “offline-to online” scenario. Although the contexts above have been described, it is important to understand that payment-capture technologies are not limited in this way. These embodiments can also be configured to work with a wide range of mobile devices, web apps, mobile apps, POS topologies and payment cards as well as computer networks and environments.

In this disclosure, devices that are operating in an online or offline mode will be referred to. The implementation may determine whether a device is in an offline or online mode. In some cases, offline mode is used to describe a state in which the device cannot connect or communicate with another device. Offline in relation to the other device, with which it is unable to connect or communicate. The offline mode can be selective or total in some cases. A device in offline mode can be a phone that is not within range of the radio base station or one that is disconnected from a network. A device that is a part of an ad hoc network and is experiencing temporary network partition due to a connectivity problem of another device within the ad hoc network. “In some embodiments, the device is operating in offline mode when it can communicate with another device within its vicinity through a peer-to-peer or short-range network (typically under 100 meters), and/or a low-power wireless communication network such as Bluetooth Low Energy, standard Bluetooth, WiFi, Near Field Communication, or Radio-Frequency Identification.

In some cases, a device can be in online mode if it is capable of communicating or connecting with another device or server via a long-range network. The online mode can be either total or selective, just like the offline mode. Online mode can be a device which can communicate through a network such as Internet, or a network such as LAN, WAN, Metropolitan Area Network, Storage Area Network, System Area Network, Server Area Network, Small Area Network, Personal Area Network, Desk Area Network, Controller Area Network, Cluster Area Network, Cloud-Based Network, etc.

In some cases, a device can operate in both online mode and offline mode. An offline device can establish a short-range channel of communication with another device that is offline, and this continues even when both devices switch to the online mode. To connect to remote devices (e.g. payment processor), the devices always require a long-range communication channel. The payment processor may be close to the devices in some cases and therefore can connect with them through a short-range communication channel.

As used in this document, “a merchant” can include any business that offers goods or services to customers. The actions attributed to the merchant can be performed by its employees, owners or agents. No distinction is made in this document unless it is specifically mentioned. As used in this document, a “customer” can also include any entity who acquires goods or service from a merchant by renting, borrowing, purchasing, leasing or other means. Items are used to refer to the goods and/or service offered by merchants. So, a merchant may conduct a transaction with a customer in which the customer purchases an item from the merchant in exchange for payment.

Click here to view the patent on Google Patents.